With the conflict in the Middle East and the disruption of the Strait of Hormuz, which is roiling global trade and exposing the vulnerability of the world’s main shipping corridors, Arctic routes are drawing increasing interest as potential alternatives, thanks to their ability to cut trade distances by about 20% to 40%. Yet a new Coface study shows that over the next five years their commercial potential will remain limited, even as navigation conditions shift due to climate change.

Although they do not constitute a credible substitute for containerized transport, these routes can nonetheless offer significant advantages for certain feedstock flows (including crude oil and natural gas), particularly US and Northern European exports to Asia.

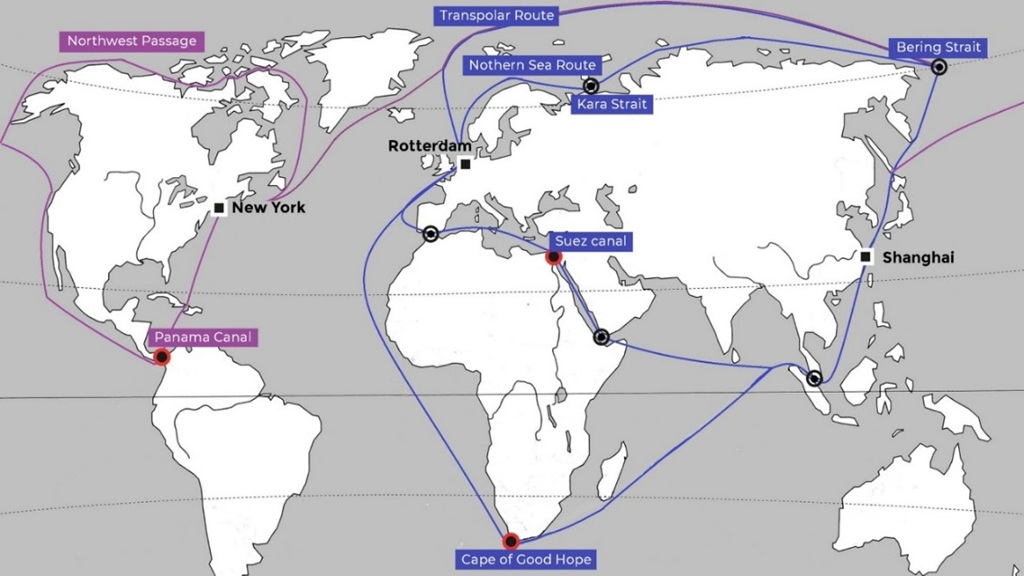

Shorter Routes in a Saturated Global Maritime System

Maritime transport accounts for 80% of world trade, concentrated among three major regions—East Asia, Europe, and North America—and organized around a limited number of strategic corridors. This concentration makes global trade especially vulnerable to geopolitical shocks.

The disruptions observed in recent months in the Red Sea, combined with tensions around the Strait of Hormuz and shifts in international trade policy—especially U.S. policy—highlight this vulnerability. In this context, Arctic routes appear to be a theoretical alternative, since using them would significantly shorten distances—by up to 40% between East Asia and Northern Europe, and around 20% to the East Coast of North America. Their greater navigability due to climate change raises questions about their economic viability.

Real Potential, but Focused Mainly on Bulk Transport

To assess the economic viability of these routes, Coface compared the unit transport costs on Arctic routes and traditional corridors for two main routes—East Asia–Northern Europe and East Asia–North America—and for three broad vessel categories: tankers, bulk carriers, and container ships.

The findings show that, over a five-year horizon, Arctic routes will continue to be used mainly for the transit of bulk commodities. Cost savings are particularly pronounced for liquid bulks (crude oil, diesel, methanol, or LNG), with reductions of up to 45% or 50% in certain cases. Dry bulks (grains, minerals, construction materials) could also become competitive, but mainly when ships can operate without icebreaker escort.

By contrast, container transport remains uncompetitive, despite the shorter distances. Operational constraints, limited vessel sizes, and the specific costs of navigating Arctic waters prevent containers from competing with the economies of scale enjoyed by traditional routes at this stage.

Limited Trade Impact, but Some Sectors Stand to Benefit

Overall, it is likely that only about 3.5% of trade between East Asia, Northern Europe, and North America will actually use Arctic routes. Therefore, their global impact on the world trade landscape would remain limited in the near term.

However, some sectors could benefit. This is especially true for industries tied to cereals, energy, metals, and wood.

How should the chart be read? About 7% of the value of goods exported from North America to East Asia could be moved via Arctic routes. That translates to $22 billion: $6 billion in solid bulks and $16 billion in liquid bulks.

Bulk exporters based on the U.S. Northeast coast or Northern Europe could, thus, improve their competitiveness in Asian markets thanks to lower transport costs and shorter transit times. Conversely, some competitors in South America (Brazil with iron ore, Chile with copper) or Africa (the Democratic Republic of Congo with certain minerals) could see their relative competitiveness in transport decline.

Beyond producers, some countries that rely heavily on traditional routes could also find themselves vulnerable. Egypt and Panama, where canal revenues represent a substantial portion of GDP, are particularly exposed. Some of the world’s major port hubs for Asia–Europe trade, such as Singapore or, to a lesser extent, Jebel Ali, could also see their strategic role questioned if a portion of trade flows shifts north. The risk to these hubs is, however, longer term, as Arctic container shipping is not expected to open to container traffic before 2030.

A Trade Route That Remains of Secondary Importance

While Arctic routes offer a distance advantage, their development faces significant constraints. Navigational windows remain seasonal, ice conditions remain variable and unpredictable, and the use of icebreakers is often essential.

The Arctic has thus become, in effect, a stage for growing strategic rivalry. The Northern Sea Route remains largely controlled by Russia, while China is gradually expanding its presence and polar capabilities. The United States is also seeking to bolster its influence in the region. In this context, developing Arctic routes is not merely a matter of weighing logistical costs; it also involves sovereignty, control of critical infrastructure, access to resources, and the rebalancing of power.

In the near term, the value of these routes seems more political than commercial. Until container shipping via this route becomes economically viable at scale, it is unlikely to radically alter the major global trade balances.

“Arctic sea routes are attracting attention because they shorten distances. Yet, commercial interest in the coming years remains very limited and focused mainly on commodities,” notes Eve Barré, sector economist at Coface.